Why pay thermal generators to stay online? It’s totally nuts

“The miserable change now at my end

Lament nor sorrow at; but please your thoughts

In feeding them with those my former fortunes

Wherein I lived, the greatest prince o’ the world,

The noblest; and do now not basely die”

Anthony & Cleopatra – Shakespeare

Oh

irony, thy face is black. First we hear “coal generators over charge”.

Then we hear “hang on coal generators need financial support”. Is this a

cosmic joke? Or just the normal thing in politics?ITK has had a long-held view that supply, very largely of variable renewable energy – wind and solar – is increasing faster than demand and that therefore some generators will lose market share.

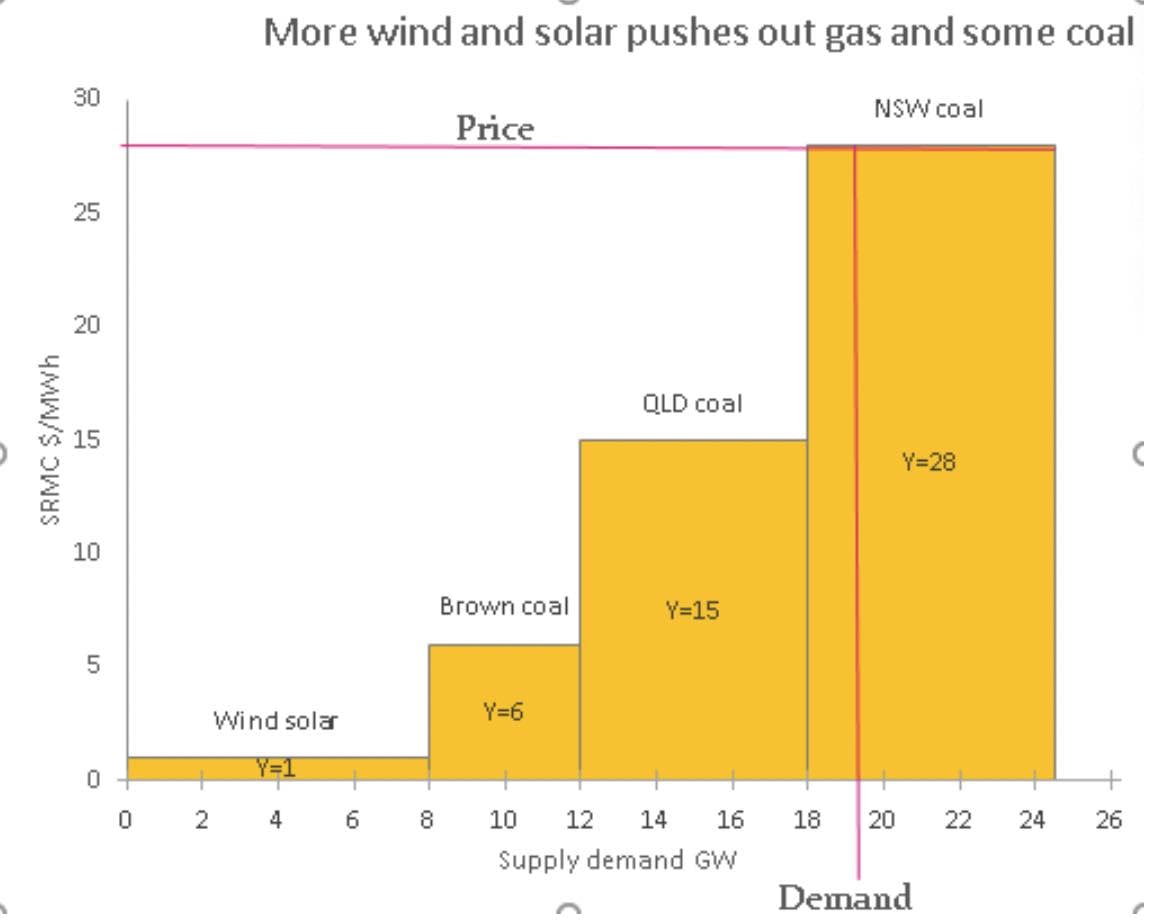

The basic economics demand that higher variable cost fuels lose share to lower variable cost fuels. The one exception is hydro, which is generally priced on a scarcity basis. See the appendix at end of this note for some simple graphs setting out the idea.

It’s beyond dispute that the high variable cost fuels are, in order: diesel generation, open cycle gas, combined cycle gas, NSW coal generation, Qld coal generation and Victoria coal generation. This has been discussed so often previously we don’t need to go there again.

Gas and NSW coal generation costs also vary over time with the international gas and coal price. Right now, the spot prices for those commodities has declined.

Even so, we anticipate that NSW coal generators will lose market share. ITK has been saying this for years.

The various outages at coal generation in other states, both Victoria and Queensland (Kogan Creek) and the careless at best and negligent at worst attention to transmission build out (until the Integrated System Plan was published) is temporarily disguising the volume pressure that will show up on NSW generators.

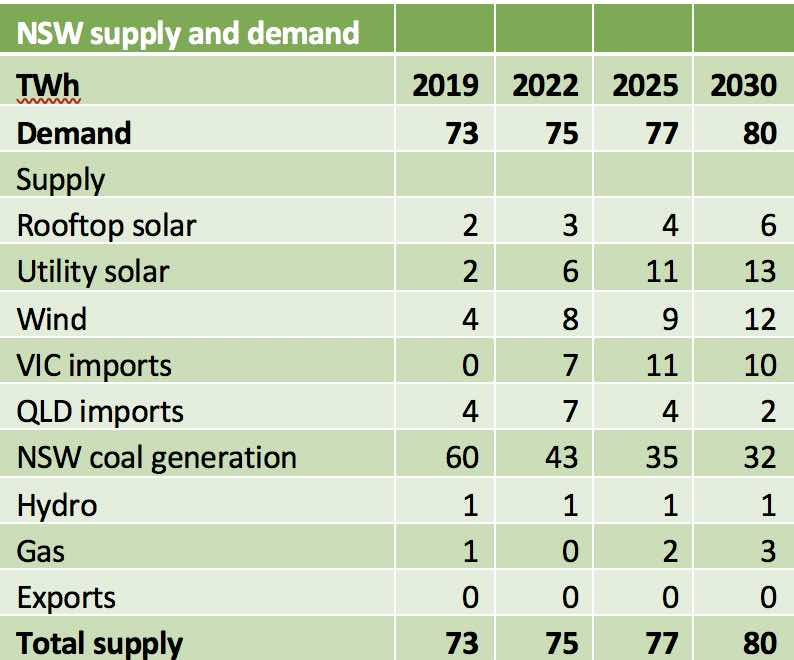

ITK’s forecast, which do allow for some unannounced new VRE supply are as follows:

We think they are some of the most aggressive forecasts in the market so more likely to be wrong than right. But we like them.

Obviously the key point is that NSW coal generators lose substantial volume

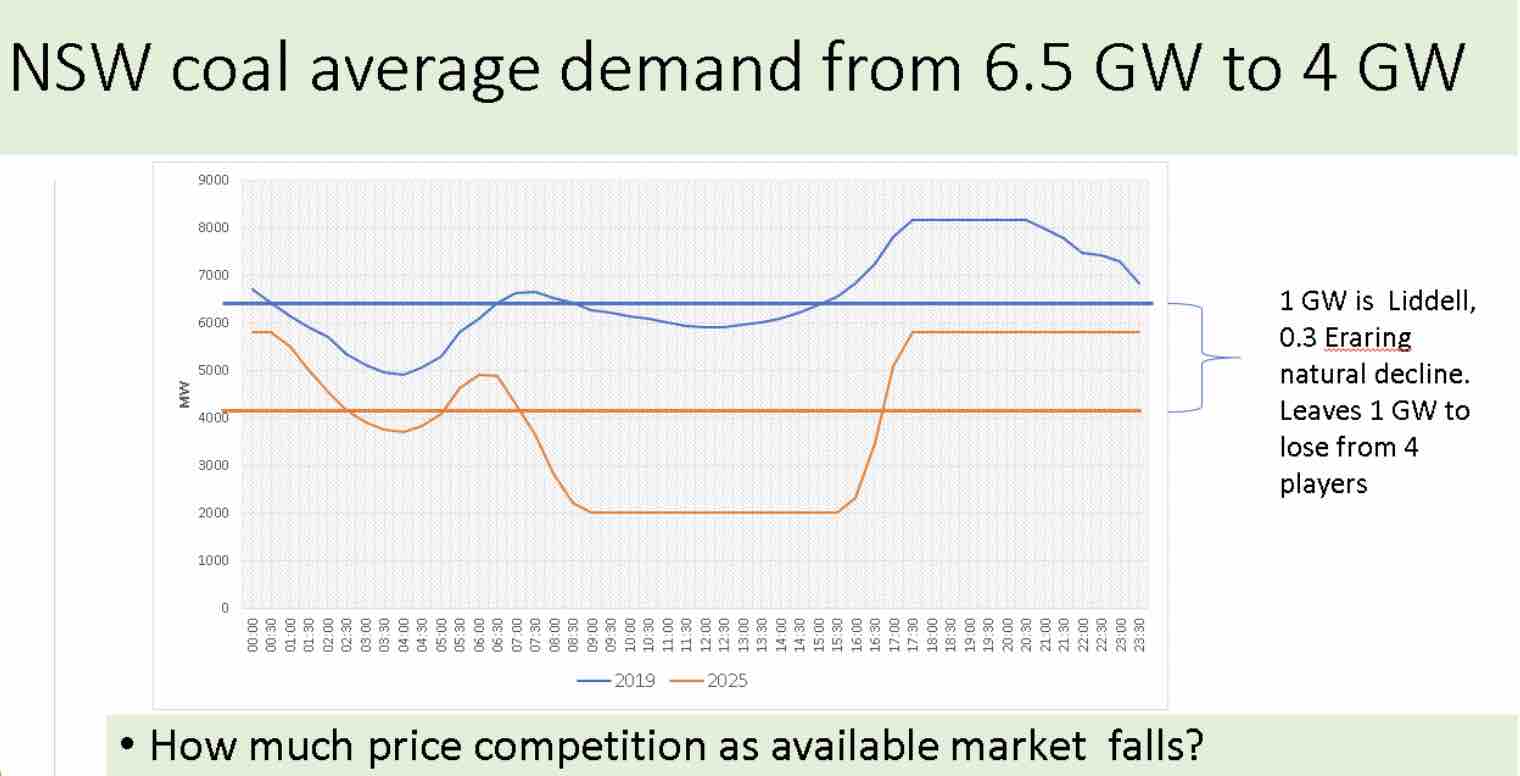

Here is a graph from a conference presentation a couple of months back that sets out ITK’s present view. It shows the average by time of day coal generation and average over the entire year.

In fact by 2025 we expect that other things, some pumped hydro, certainly some batteries, a touch of demand response, to reduce the daily peak ramp. In our view there is plenty of scope to close a second NSW generator.

Why would you pay thermal generators to stay online? It’s totally nuts.

We don’t want to get into a long discussion here about capacity vs energy markets. That’s an interesting but lengthy debate and not too much of the available evidence really supports capacity markets. In any event the NEM has a capacity market/instrument of sorts: the $300 cap.However as Gordon Wymer from Snowy, by far the largest provider of peaking services and cap cover in the NEM, said in a recent Energy Insiders podcast, Snowy is rapidly moving away from providing caps to providing firmed generation contracts.

And in fact that is what other retailers like Infigen are also doing. Here we just confine ourselves to a few blindingly obvious points.

- There is a reliability guarantee on all retailers;

- Paying ageing generators to stay on line will disincentivise any new investment providing similar services;

- You can’t run a modern, vibrant Australian or NSW economy on a fleet of clapped out 40 and then 50-year-old generators. Dumb, dumb, dumb.

- The idea is to decarbonise. To avoid 2°C warming, the world needs to get rid of its carbon emissions fairly quickly, basically the vast majority of emissions need to be gone by the early 2030s.

- I’ll say no more on this subject but the electricity industry sometimes needs reminding.

- Therefore the objective is not to pay clapped out generators such as Yallourn, or Gladstone, or Vales Point B or heaven forbid Liddell to stay online but to ensure that good policy results in enough new supply being built.

- This new supply will/should be largely VRE backed up with modest investment in firming capacity. VRE supply, if enough transmission exists, can supply 100% of the required demand 70-80% of the time according to several studies. Ie only 20-30% of the time is energy storage or firming power required.

We need a new LRET, or CET, or carbon tax.

ITK believes that Government financed reverse auctions are the cheapest way to procure new supply. (And the ACT has just announced a new one). However, we accept that given appropriate policy the market can do as good a job, possibly even better.But a policy is needed. Yes new VRE is cheaper than new build coal or gas. VRE is increasingly competitive with existing coal on cost.

Cost, however, is far from the only investment driver.

Who would build a solar plant in today’s market? No transmission, endless bureaucracy in getting connected and price in the middle of the day is close to zero. This is far more of a problem for the NEM than the fact that some coal generator may close early.

It’s not quite the same for wind but there are still lots of issues.

50% VRE policy by 2030 is the obvious answer

On the other hand if there was a policy dictating, say 50% VRE by 2030, then these problems would be solved. Why?A 50% VRE policy would make even the most obstinate regulator see that new transmission needs to be built and more needs to be done to make renewable energy zones hum.

A 50% VRE policy would provide a strong investment signal to pumped hydro and batter developers that they would get some energy in the middle of the day and lead to partnerships such as Snowy 2.0 and its 880 MW of VRE contracts. A solar farm would get a low but guaranteed price and the energy would end up in the evening peak market.

A 50% VRE policy would bring forward some coal closures and allow the AEMO and everyone else to plan for the future with more confidence.

In addition, given existing policy in Victoria and Queensland the share of renewables in Tasmania and South Australia it’s really only NSW that needs to adopt such a policy. And, of course, for the transmission industry to build the blasted transmission.

Appendix – short run variable cost presented statistically

The first graph shows how high marginal cost gas generation often sets the electricity price in the NEM. The cost numbers are on the lower side for coal, but don’t change the principle.There is nothing at all new in these graphs, they simply illustrate a cost based bid stack and the impact of new lower variable cost supply.

David Leitch is a regular contributor to Renew Economy.

He is principal at ITK, specialising in analysis of electricity, gas

and decarbonisation drawn from 33 years experience in stockbroking

research & analysis for UBS, JPMorgan and predecessor firms.

-

UNSW report proposes floating microgrids of electric boatsby Lisa Cohn on 12 September 2019 at 11:37 AM

-

Power Ledger trials P2P solar trading platform in first regional settingby Sophie Vorrath on 10 September 2019 at 3:16 PM

-

Tesla slashes price of Powerwall 2 battery by $2,000 for VPP customersby Sophie Vorrath on 6 September 2019 at 3:26 PM

-

Tesla at Nürburgring update: Video, delays, seven seats and driver discussionsby Bridie Schmidt on 13 September 2019 at 1:08 PM

-

Formula E attracts young audience as revenue and popularity growby Bridie Schmidt on 13 September 2019 at 12:07 PM

-

On the road: Electric drive week expands to Victoria, Australiaby Bryce Gaton on 13 September 2019 at 11:55 AM

We Recommend

Neoen unveils massive wind, solar battery project ...Governments,Renewables,Solar,Storage

Solar farms switch off en masse as coal plants fle...CleanTech Bites,Coal,Governments,Solar

CSIRO to co-develop high energy, highly safe EV ba...Electric Vehicles,Research Groups, Institutes and Universities,Storage

Wind overtaking brown coal is only a matter of tim...Coal,Markets,Renewables

EDL’s Coober Pedy Hybrid Renewable Project wins at...Press Releases

Brigalow solar farm caught up in Queensland bush f...Climate,Governments,Solar

{kind=link}

{kind=link}

No comments:

Post a Comment