Shanghai-based Wison Engineering to carry out urgent repairs

Venezuela to pay for services with diesel fuel in barter deal

Sign up for Next China, a weekly dispatch on where the country stands now and where it's going next.

A

Chinese contractor has agreed to shore up Venezuela’s derelict refining

network to ease fuel shortages, potentially complicating the Trump

administration’s push for regime change in the oil-rich country.

Wison Engineering Services Co.,

a Shanghai-based chemical engineering and construction company that is

using China’s ‘Belt and Road’ infrastructure program to expand overseas,

agreed last month to repair Venezuela’s main refineries in exchange for

oil products including diesel, according to people with knowledge of

the deal.

U.S. financial sanctions aimed at starving the current regime

of revenue contributed to the decision to revive a domestic refining

industry crippled by years of mismanagement and under-investment, said

one of the people, who asked not to be identified because the

information is confidential.

Venezuelan President Nicolas Maduro (2-R) shakes hands with China’s Xi Jinping (2-L) in Caracas

LEO RAMIREZ/AFP/Getty Images

The

deal mirrors the OPEC producer’s other arrangements with Russian and

Chinese oil majors, under which payments are made in crude by

Venezuela’s cash-strapped national oil company.

Wison’s repairs are expected to last six months to a year,

according to another person. The Nicolas Maduro administration was

having difficulties navigating the U.S. economic blockade even before

the U.S. announced additional restrictions on Aug. 5. Last month state-controlled Petroleos de Venezuela SA was importing Russian gasoline through Malta to relieve shortages, a slow and expensive route to the Caribbean nation.

Irregular Supply

Irregular

fuel supplies have crippled mobility in a country where shortages of

food and basic medical supplies have already caused a health crisis and

led to one of the largest mass migrations of recent times. PDVSA, as the

state producer is known, has been directing most available gasoline to

Caracas, where Maduro is most vulnerable to mass protests.

The

Trump administration was hoping to swiftly chase Maduro out of power

earlier this year, and has criticized China and Russia for supporting

what it considers a criminal and repressive regime.

Wison didn’t respond to an email or fax seeking comment on

the refinery contract. PDVSA didn’t respond to emails and calls seeking

comment.

The Chinese company hasn’t completed a contract it won in

2012 to overhaul the Puerto la Cruz refinery. Wison’s revenue from

Venezuela sank 72% last year as the nation’s economic crisis deepened,

according to it’s annual report.

China and Russia have an interest

in preventing the complete collapse of Venezuela’s oil industry because

it’s the only way to recoup the tens of billions of dollars in loans

and investments they have made in the past decade. Wison’s deal also

underscores how the oil-hungry Asian nation remains committed to

Venezuela as a strategic location for foreign investment.

Economic Blockade

Restoring

fuel production, if it happens fast enough, would weaken the U.S.

economic blockade and put Maduro in a stronger negotiating position as

talks with the opposition drag on without any visible progress.

Despite

Venezuelans’ widespread dissatisfaction with their government,

divisions within the opposition are complicating the push toward a

post-Maduro administration. While about 50 nations recognize National

Assembly President Juan Guaido as the country’s interim president, China

has declined to get involved in what it considers an internal conflict.

Venezuela’s

refining industry, once a major supplier to the U.S. with 1.3 million

barrels a day of capacity, has been in gradual decline due to theft,

inadequate maintenance and a brain drain of qualified staff, and was hit

by a series of major power outages this year. In recent years, PDVSA

hasn’t even been able to meet domestic gasoline demand that has

historically been about 250,000 barrels a day.

The U.S. has so far shied away from military intervention in

Venezuela and has instead imposed economic sanctions that target the oil

industry and key members of the government and the military. American

officials continue to project confidence about replacing Maduro with a

pro-business administration despite the lack of progress.

China

rejects “foreign interventions and unilateral sanctions” in Venezuela,

and supports dialogue between the government and the opposition, its

embassy in Caracas said in a statement on May 12. The embassy didn’t

immediately offer additional comments when contacted by Bloomberg.

China wants “to be identified with a friendly socialist

government, especially in the backyard of the U.S.,” said Schreiner

Parker, Rystad Energy’s vice president for Latin America. “They have no

guarantee that a regime change will necessarily mean that they’re going

to be repaid.” — With assistance by Lucia Kassai, and Alfred Cang

UP NEXT

China Yuan-Fixing Drama Fades as PBOC Seen Pursuing Stability

markets

China Sets Yuan Fixing Stronger Than Expected, Soothing Nerves

Tian Chen

Updated on

PBOC reinforcing message it is seeking stability, analyst says

Reference rate set weaker than 7 for the first time since 2008

Why the U.S. Calls China a Currency Manipulator

Sign up for Next China, a weekly dispatch on where the country stands now and where it's going next.

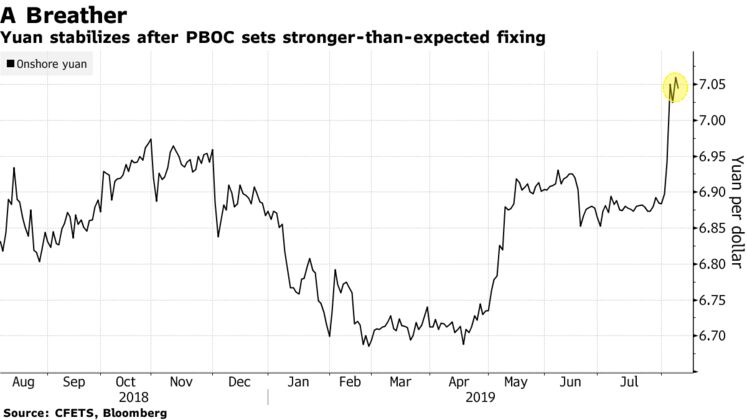

The

yuan steadied on Thursday after China’s central bank set the daily

fixing stronger than analysts expected, providing some reassurance to

traders rattled by a tumultuous week in markets.

The

currency rose as much as 0.3% after the People’s Bank of China set its

daily reference rate at 7.0039 per dollar. While that was the first time

since 2008 that the fixing was weaker than 7, it tracked earlier moves

in the spot rate and was stronger than the 7.0156 average estimate of 21

analysts and traders surveyed by Bloomberg.

The fixing has become a closely-watched event after a weak

reference rate on Monday triggered the biggest loss in the yuan since

2015, sparking concern about a global currency war. The latest move

comes after the PBOC took steps to calm sentiment, including reassuring

foreign companies that the yuan won’t weaken significantly.

“China wants to prevent panic now,” said Gao Qi, a strategist

at Scotiabank. “The PBOC will continue to send signals to stabilize the

yuan in the near term.”

The yuan is down 3.7% in the past three months, and at its lowest since at least 2015 against a basket of 24 trading partners’ currencies.

Further depreciation is still on the cards. U.S. President

Donald Trump has threatened to impose more tariffs on Chinese goods and

the PBOC could loosen its monetary policy to aid growth. Central banks

in New Zealand, India and Thailand all made surprise interest-rate cuts

on Wednesday, stoking fears of a full-on currency war.

Yet China

will be keen to avoid the experiences of 2015-2016, when a one-off

devaluation spurred companies and individuals to yank money out of the

country.

“I suspect the authorities will want to gain more comfort

over the next few days and weeks that we’re not seeing a huge

intensification of capital outflow pressures, before they possibly allow

it to go a little weaker,” said Andrew Tilton, chief Asia Pacific

economist at Goldman Sachs Group Inc. “Right now I suspect they want to

desensitize the market to this magic number of 7, and make sure that

they are not going to have a capital outflow problem.”

The

risk is how the Trump administration responds to a weaker yuan. The

U.S. this week labeled China a currency manipulator, a formal

designation which China rejects. The yuan may tumble to as weak as 7.7

in the event of an intensification of trade tensions, according to

Societe Generale SA.

“The further it falls, the more likely the

Trump administration will respond with more tariffs and other policies

to target China,” said Ben Emons, managing director for global macro

strategy at Medley Global Advisors in New York. “All of which points to

even more downside in the RMB, which is then a problem for other

emerging countries that compete with China,” he said, using an

abbreviation of the yuan’s official name.

That means the PBOC’s reference rate is going to continue to be closely watched by traders and central bankers alike.

“The

fix is the number one game in town and will continue to dictate the

pace of play for risk assets over the near-term,” said Stephen Innes,

managing director for VM Markets Ltd. in Singapore. “Nothing else

matters at this stage.” — With assistance by Qizi Sun, Enda Curran, and Claire Che

(An earlier version of the story corrected a spelling error in the headline.)

No comments:

Post a Comment